The Federal Reserve’s pause in rate cuts at this meeting is no longer in doubt; the real debate lies in whether the pause is “dovish” or “hawkish.” Both Morgan Stanley and Bank of America expect Powell to signal a dovish stance. If the forward guidance retains language about “considering further adjustments to the target range,” it implies the easing window remains open. This article is sourced from Wall Street Journal, organized, translated, and written by Foresight News.

(Background summary: The US dollar index hits a “four-year low”—why is Trump not worried? The Fed is 97% unlikely to cut rates tonight.)

(Additional context: US Q3 2025 economy surges with GDP up 4.4%! Core PCE rebounds, dampening expectations of rate cuts, Bitcoin briefly drops below $90,000.)

Table of Contents

- Rate pause confirmed, market focuses on forward guidance

- Slight language adjustments in statement send key signals

- Powell press conference: three key points to watch

- Political pressure may become an “unsolvable issue”

- This year’s rate cut path: divergence remains significant

- Market impact: limited volatility as baseline scenario

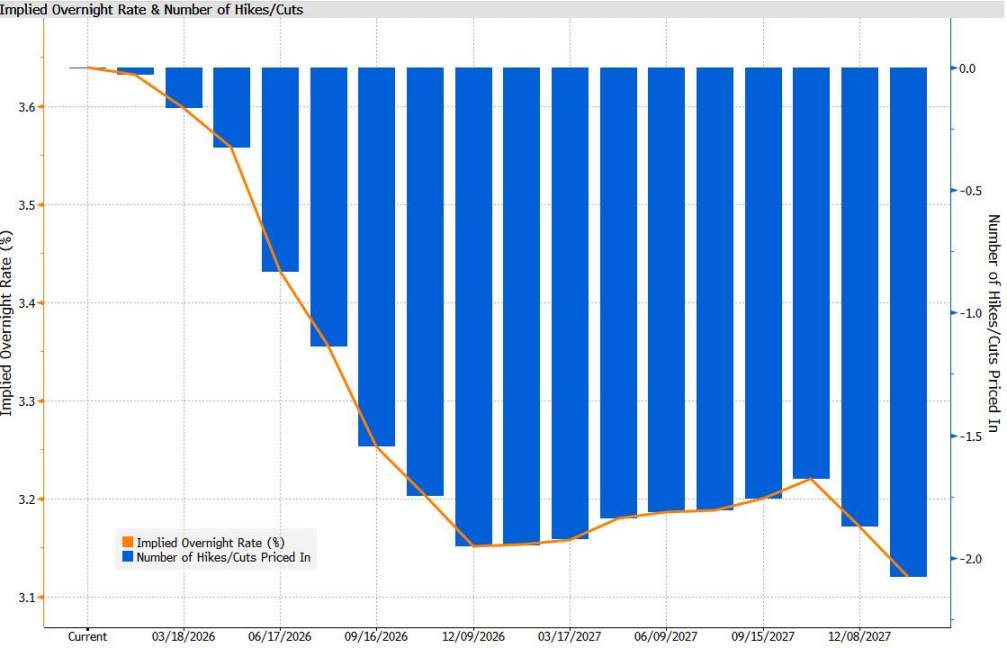

The market has fully priced in the Fed’s expectation to keep rates steady at 3.50-3.75%, shifting focus to whether this is a “dovish pause” or a “hawkish pause.”

For investors, the key is whether Powell will retain forward guidance about “considering further adjustments to the target range,” indicating a continued easing bias, or revert to “considering any adjustments to the target range,” implying a longer pause and a hawkish stance. As unemployment drops to 4.4% and economic activity remains solid, the market has delayed its first rate cut expectation to July, with an entire year’s cut pricing of only 45 basis points. Divisions within the committee remain serious, with Director Miran expected to vote against again.

Rate pause confirmed, market focuses on forward guidance

According to the latest surveys by Bloomberg and Reuters, all surveyed economists expect the Fed to keep rates unchanged at this meeting, with 58% expecting rates to remain steady throughout Q1. The current pricing in the money markets suggests about 45 basis points of rate cuts by year-end, with the first 25 basis point cut possibly as early as July.

Goldman Sachs describes this meeting as “uneventful,” expecting no change to the federal funds rate, with only minor adjustments to the statement and little guidance on future policy paths.

Morgan Stanley explicitly expects the Fed to signal a “dovish pause”—recent stabilization in the labor market and steady economic data are the main drivers for pausing rate cuts, but confidence in inflation falling later this year will keep the Fed leaning towards easing.

Slight language adjustments in statement send key signals

Institutions generally expect multiple adjustments in the statement. Morgan Stanley predicts the committee will upgrade its assessment of economic growth from “moderate” to “solid.” More importantly, it is expected to remove the phrase about “increased downside risks to employment”—since choosing to pause rate cuts logically suggests concerns about the labor market have eased.

Barclays shares a similar view, expecting the statement to mention “employment growth slowed last year, and the unemployment rate rose slightly,” but to omit “recent indicators are consistent with these developments.” Regarding inflation, despite recent core PCE data being relatively mild, distorted by government shutdown effects, the statement is still expected to maintain that “inflation has increased over the past few months and remains somewhat elevated.”

The most critical forward guidance, market expects, will retain language like “considering the range of possible adjustments to the target,” implying an easing bias remains, constituting a “dovish pause.” If it reverts to “considering any adjustments to the target range,” it would suggest a longer pause, a hawkish stance.

Powell press conference: three key points to watch

U.S. Bank Securities notes that, relative to recent rate repricing, Powell’s press conference may lean dovish. Analysts will focus on three areas:

- Labor market assessment: Whether Powell emphasizes the December unemployment rate dropping to 4.4% or downplays it as just one month’s data. Equally important is whether Powell reaffirms tolerance for a slight increase in unemployment. In December, Powell said that after a 75 basis point rate cut, the policy stance “should be able to keep the labor market stable or unemployment only rise by one to two tenths.”

- Inflation trend analysis: Market reactions will depend on whether Powell emphasizes the December core PCE YoY at about 3%, or ongoing housing deflation and tariff-driven inflation below expectations. Citi forecasts core PCE at 2.8% in Q4 2025, below the median forecast of 3.0% in the December SEP.

- Neutral rate judgment: Investors should watch Powell’s comments on the neutral interest rate. In December, Powell said the policy rate “is within a reasonable estimate of the neutral rate.” Any change in wording about the neutral rate, or a stronger emphasis on productivity improvements, will be noteworthy.

Political pressure may become an “unsolvable issue”

Nick Timiraos of the “New Federal Reserve Communications” reports that, despite the Fed being in a wait-and-see mode, the White House is exerting unprecedented political pressure.

This month, the U.S. Department of Justice launched a criminal investigation into Powell. Last week, the Supreme Court heard oral arguments on whether Trump has the authority to dismiss Fed Board member Cook, with several justices expressing doubt over whether the president has that power.

Analysts generally expect Powell to face numerous politically related questions at the press conference, but he is likely to respond with “no comment,” reaffirming the Fed’s independence in monetary policy decisions.

Bank of America Securities explicitly states, “More politically oriented questions may dominate the press conference, but Chairman Powell is likely to avoid providing answers.”

This year’s rate cut path: divergence remains significant

Regarding this year’s rate cut trajectory, there are clear disagreements among institutions. Goldman Sachs expects two 25 basis point cuts in June and September, bringing rates down to 3.00-3.25%. Barclays expects two cuts in June and December. Citi forecasts a total of 75 basis points of cuts in March, July, and September.

Morgan Stanley notes that among 19 Fed officials in the December meeting, 12 expect at least one more rate cut this year, but that cut was opposed by two officials, and some supporting cuts have reservations. This suggests the threshold for further cuts has risen, and the Fed leadership likely aims to build a stronger consensus than in December last year.

Timiraos analyzes that to cut before mid-year, the labor market would almost certainly need to worsen, as inflation decline may not be fast enough to persuade skeptical officials beforehand. Over the past 18 months, inflation has made little substantive progress.

Market impact: limited volatility as baseline scenario

Regarding market impact, institutions generally expect limited price fluctuations from this meeting.

U.S. Bank Securities states, “Market expectations for the January FOMC meeting are quite limited. The market is almost fully priced for rates to remain at 3.5-3.75%.” They expect, aside from standard volatility after the statement and press conference, limited net price movement.

In the forex market, U.S. Bank notes that during the FOMC meetings this cycle that kept rates unchanged, EUR/USD performance mostly stayed within about ±0.2%, with an average close to zero. “Unless there are major surprises—which seem unlikely—this meeting may produce limited net price action.”

It is noteworthy that at least one dissenting vote is expected, from Fed Board member Stephen Miran, who has advocated for more aggressive easing at every meeting since joining the committee last September. The institution expects him to vote for a 25 or 50 basis point rate cut. This will be the fifth consecutive meeting with a dissent, highlighting ongoing divisions within the committee.

Additionally, Directors Bowman and Waller may also vote for rate cuts, given their higher concern about the labor market than some colleagues.

Timiraos emphasizes that Waller’s vote will be particularly scrutinized. He is one of the potential successors Trump is considering to replace Powell. If he votes for a rate cut, it could boost his prospects; if he votes to keep rates unchanged along with the majority, it may reinforce his image as an independent voice but could also reduce his chances of becoming Fed Chair.